Comparison Between Internal vs External Audits

The words “internal audit” often conjure a sense of fear, frustration, and time consumption. Even in the best circumstances, most would find having someone review their activities unsettling or intimidating. Having an understanding of the role of an internal audit, knowing what to expect during an internal audit, and knowing potential pitfalls to avoid will help put you at ease and make a much more pleasant and valuable experience.

What is Internal Audit?

Internal vs External Audits: How are They Different?

Who Performs the Audit?

- Internal Audits – Internal Auditors, typically employees of the company

- External Audits – External Auditors, typically members of a CPA firm

Who is the Audit Reported to?

- Internal Audits – Board of Directors, and members of management

- External Audits – Shareholders and members outside of the company

What Does the Audit Cover?

- Internal Audits – Internal Controls related to:

- Governance

- Risk Management

- Process Improvement

- Governance

- External Audits – Financial Reports, and Internal Controls related to Financial Reporting

Why is the Audit Performed?

- Internal Audits – To assess and improve the effectiveness of governance, risk management, and control over critical processes. To provide the board and management with information and assurance related to their duties.

- External Audits – To validate, or provide reasonable assurance, the material accuracy of financial reports from the organization to its stakeholders.

When are Results Reported by the Audit?

- Internal Audits – May report at any frequency designated by the Board

- External Audits – Annually

Why Do Organizations Have Internal Audit?

The executives of publicly traded companies legally responsible for the accuracy of its financial statements and the internal controls over financial reporting. Internal Audit functions play a critical role in helping executives to reach their conclusions. Also, Internal Audit efforts to identify breakdowns in internal controls helps safeguard against potential fraud, waste or abuse, and ensure compliance with laws and regulations.

What Value does Internal Audit Provide to an Organization?

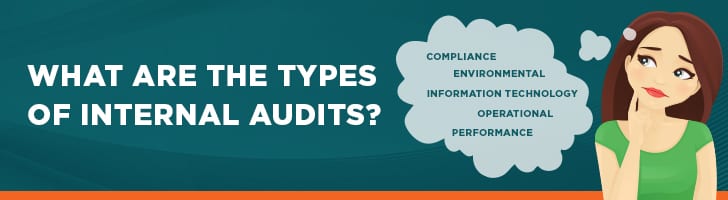

What are the Types of Internal Audits?

While a significant portion of internal audit covers internal controls over financial reporting within the organization as they pertain to generally accepted accounting procedures (GAAP) impacting their financial statements. Many organizations also recognize the need for other types of assessments or audits outside of accounting or finance. Some of these key areas include compliance (i.e., regulatory), environmental, information technology, operational and performance audits.

- Compliance Audits evaluate compliance with applicable laws, regulations, policies and procedures. Some of these regulations may have a significant impact on the company’s financial well-being. Failure to comply with some laws, such as the Foreign Corrupt Practices Act (FCPA) or General Data Protection Regulation (GDPR), may result in millions of dollars in fines or preclude a company from doing business in certain jurisdictions. Here is a link to a beginners guide to GDPR.

- Environmental Audits assess the impact of a company’s operations on the environment. They may also assess the company’s compliance with environmental laws and regulations.

- Information Technology Audits may evaluate information systems and the underlying infrastructure to ensure the accuracy of their processing, the security and confidential customer information or intellectual property. They will typically include the assessment of general IT controls related logical access, change management, system operations, and backup and recovery.

- Operational Audits assess the organization’s control mechanisms for their overall efficiency and reliability.

- Performance Audits evaluate whether the organization is meeting the metrics set by management in order to achieve the goals and objectives set forth by the Board of Directors.

What is the Internal Audit Procedure / Process?

An internal audit should have four general phases of activities—Planning, Fieldwork, Reporting, and Follow-up. The following provides a brief synopsis of each phase.

- Planning – During the planning process, the internal audit team will define the scope and objectives, review guidance relevant to audit (e.g., laws, regulations, industry standards, company policies and procedures, etc.), review the results from previous audits, set a timeline and budget for the audit, create an audit plan to be executed, identify the process owners to involve, and schedule a kick-off meeting to commence the audit.

- Fieldwork – Fieldwork is the actual act of auditing. Throughout this phase, the audit team will execute the audit plan. This usually includes interviewing key personnel to confirm an understanding of the process and controls, reviewing relevant documents and artifacts for an example execution of the controls, testing the controls for a sample over a period of time, documenting the work performed, and identifying exceptions and recommendations.

- Reporting – As you might guess, internal audit will draft the audit report during the reporting phase. The report should be written clearly and succinctly to avoid misinterpretation and to encourage the intended audience to actually read and understand the report. Findings should be accompanied by recommendations that are actionable and lead directly to process improvements. The process of issuing an internal audit report should include drafting the report, review the draft with management to ensure the accuracy of findings, and issuance and distribution of the final report.

- Follow-up – The final stage is an important one that is often overlooked and neglected. Following up is critical to ensure that the recommendations have been implemented to address the findings identified. This process should include appropriate follow-up with process owners needing to implement the recommendations as well as Board oversight of the company’s overall status in addressing findings identified by internal audit. If an organization fails to follow-up on the implementation of recommendations, it is unlikely that the changes will be made.

What are Common Pitfalls that can Derail an Internal Audit?

An internal audit can be extremely useful to help streamline processes, find gaps and identify fraud. However, my experience as an auditor has taught me to recognize the red flags that can quickly derail the process.

- Scope creep: Proper planning and definition of scope is key to a successful internal audit. With complex systems and workflows, it is easy for the scope to expand rapidly. Be sure to proactively plan for when an issue occurs that may affect scope, so that the team can respond quickly and efficiently (e.g. do you ignore the issue, add to it, put it off until later). When scope starts to expand, be sure to pump the brakes and reassess; nothing is worse than allowing the scope to increase and later realizing that you are one step away from basically auditing the entire organization and all the processes.

- Not talking to all clients/stakeholders: Be sure to involve your client and stakeholders early and often. I recommend going deeper than managers or team leads; talk with the staff, engineers, etc. Many times, the “people in the trenches” may be following a completely different process than what is documented or understood by management.

- Not reviewing the data: When data is needed, it’s typical to ask the team you are auditing to provide it, but how do you know that the data is accurate? Was the data modified, trimmed or altered in any way? If possible, sit with the DBA or data provider to understand how the data is being generated. Always ask questions and try to get data that has been generated directly from the system, along with the queries or constraints used to generate it.

- Objectivity and Independence: This is especially difficult in a smaller organization. In a larger organization, internal auditors report to a board of directors or an audit committee, but in smaller companies, an internal auditor may be reporting to the same person or group they are auditing. The key is to stay objective, independent and have a forward looking mindset. Remember that an internal auditor is trying to help and should be allowed to do so even if the results are hard to hear.

What are the Professional Standards in an Internal Audit?

The Institute of Internal Auditors (IIA) has set the internationally recognized framework for internal auditing. It is called the International Professional Practices Framework (IPPF). The IPPF provides “mandatory” and “strongly recommended” guidance. These are standards that apply are applied by over 160,000 internal auditors who are working globally within the framework.

Conclusion

I hope you this has helped you to better understand the role of internal audit, anticipate the process in your next internal audit, and avoid the potential pitfalls that can derail an internal audit. For more information on this visit TAXAJ.

Related Articles

What are Operational Audits & How is it Performed?

What Are Operational Audits? “A systematic process of evaluating an organization's effectiveness, efficiency and economy of operations under management's control and reporting to appropriate persons the results of the evaluation along with ...What is External Audit & When is it Applicable in India?

What is External Audit? External Audit is defined as the audit of the financial records of the company in which independent auditors perform the task of examining validity of financial records of the company carefully in order to find out if there is ...Nonprofit Organization Audits in Bangalore

Introduction: In the bustling city of Bangalore, nonprofit organizations play a crucial role in addressing societal needs, ranging from education and healthcare to environmental conservation and poverty alleviation. To ensure transparency, ...Annual Audit In India

An annual audit in India refers to the process of examining and evaluating a company's financial records, statements, and transactions to ensure accuracy, compliance with accounting standards, and adherence to applicable laws and regulations. It is a ...How to conduct a Proper Financial Audit?

What Is a Financial Audit? A financial audit is the investigation of your business’ financial statements and accompanying documentation and processes, and is performed by someone who is independent of your organization. These often-annual events ...