Letter Of Undertaking Under GST

File Letter of Undertaking (LUT) in GST

What does LUT under GST means?

LUT in GST: Full form/meaning is Letter of Undertaking. It is prescribed to be furnished in the form GST RFD 11 under rule 96 A, whereby the exporter declares that he or she will fulfill all the requirement that is prescribed under GST while exporting without making IGST payment.

Who needs to file LUT in Form GST RFD-11?

GST LUT is to be submitted by all GST registered goods and service exporters. The exporters who have been prosecuted for any offense and the tax evasions exceeding Rs 250 lakhs under CGST Act or the Integrated Goods and Service Act, 2017 or any existing laws are not eligible to file the GST LUT. In such cases, they would have to furnish an Export bond.

Here the motive of the government was to expand the export base by providing reliefs on exports. GST experts from TAXAJ can help you with GST LUT filing or Export bond Filing.

Under CGST Rules,2017, any registered person can furnish an Export bond or LUT in GST RFD 11 without paying the integrated tax. They can apply for LUT if:

- They intend to supply goods or services to India or overseas or SEZs

- Are registered under GST

- They wish to supply goods without paying the integrated tax.

Documents Required for LUT under GST

An LUT can be submitted by any individual who is registered under GST provided he has not been executed in case of tax evasion exceeding Rs.250 lakh or any other offense.

- LUT cover letter - request for acceptance - duly signed by an authorized person

- Copy of GST registration

- PAN card of the entity

- KYC of the authorized person/signatory

- GST RFD11 form

- Copy of the IEC code

- Canceled Cheque

- Authorized letter

Process for Filing LUT in GST?

To file a Letter of Undertaking (LUT) in a case where the exports are made without payment of taxes, below are the steps on how to file and furnish bonds when the exports are made without payment of taxes.

1 Check the furnishing and jurisdiction requirements. If a bond is to be filed, additional documents relating to the bank guarantee must be prepared.

2 Prepare necessary documents for Bonds. Following documents are to be filed for bonds:

For Bonds:

Form RFD-11

Bond on stamp paper

Bank guarantee

Authority letter

Other supporting documents

A separate bond is not needed to be furnished for each consignment. Instead, he can furnish a running bond. A running bond helps the exporter to carry forward the same terms and conditions in the bond for the next consignment.

3) A duplicate copy should be prepared along with an official document.

4) The next step is to submit the documents to the department and get the same verified by a relevant officer to avoid any rejection

5 After filing the document, a signed letter shall be issued by the officer acknowledging the same.

Eligibility for Filing LUT in GST

Any registered taxpayer who is into exporting goods and services can make use of Letter of Undertaking. Any person who has been prosecuted for tax evasion for an amount of Rs. 250 lakh or above are ineligible.

The validity of such LUT's is for one year, and an exporter is required to furnish a fresh LUT for each financial year. If the conditions mentioned in the LUTs are not satisfied within the specified time limit, then the privileges will be revoked, and the exporter will have to furnish bonds.

Other assesses should furnish bonds if the export is being made without the payment of IGST. LUTs / Bonds can be used for:

- Zero-rated supply to SEZ without payment of IGST

- Export of goods to a country outside India without the payment of IGST.

- It is providing services to a client in a country outside India without paying IGST.

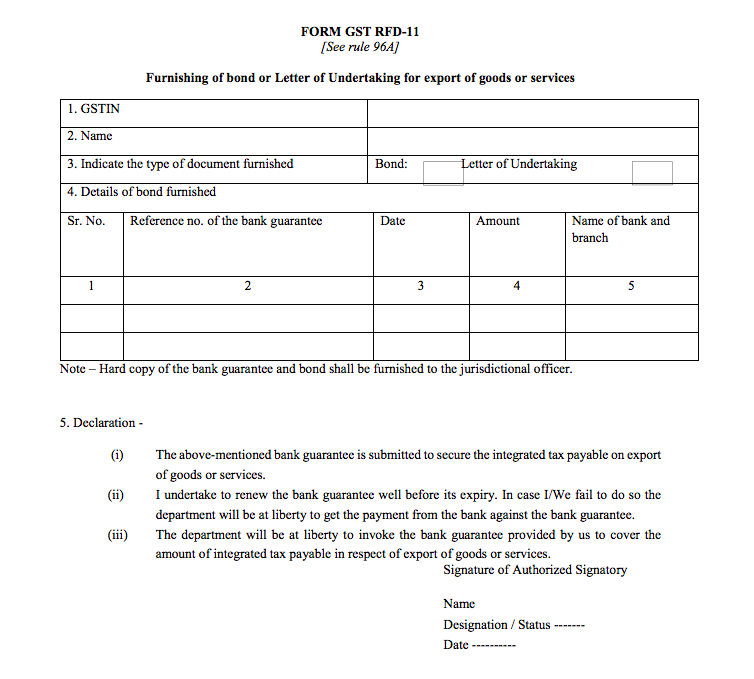

Filing of Letter of Undertaking (FORM GST RFD-11)

The Form RFD-11 is filed in the format below:

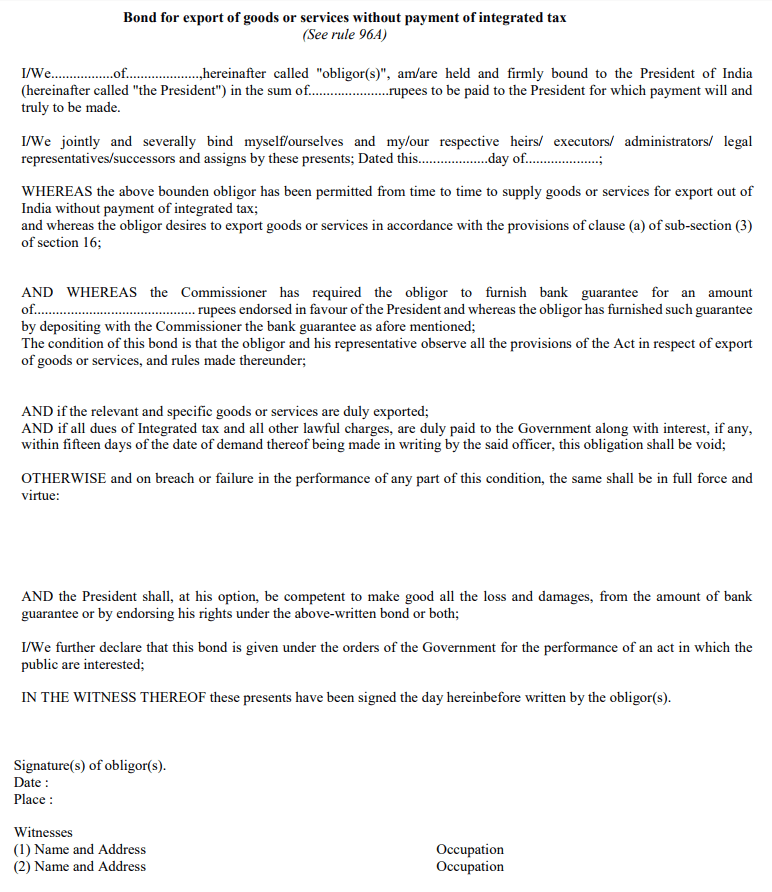

Export Bond for GST

Entities that are not eligible to submit a Letter of Undertaking based on the conditions mentioned will have to furnish an export bond and a bank guarantee. The applicant needs to cover the amount of tax involved in the export based on estimated tax liability self-assessment.

Export bond should be furnished on non-judicial stamp paper of the value as applicable in the State in which the bond is being furnished.

Also, exporters can furnish a running bond, so that export bond needs not to be executed for each export transaction. However, if the outstanding tax liability on exports exceeds the bond amount at any time, then the exporter must furnish a new bond to cover the additional liability.

A bank guarantee can be mandated along with an export bond. The value of the bank guarantee should usually not exceed 15% of the bond amount. However, based on the exporter's track record, the bank guarantee required to be submitted with the export bond can be waived off by the jurisdictional GST Commissioner.

Form for Bonds:

- Registered Name

- Address

- Amount of bond furnished.

- Date of furnishing

- Amount of bank guarantee furnished.

- Signature, date, and place

- Details of witnesses (Name, address, and occupation)

Created & Posted By Ravi Kumar

CA Article at TAXAJ

TAXAJ is a consortium of CA, CS, Advocates & Professionals from specific fields to provide you a One Stop Solution for all your Business, Financial, Taxation & Legal Matters under One Roof. Some of them are: Launch Your Start-Up Company/Business, Trademark & Brand Registration, Digital Marketing, E-Stamp Paper Online, Closure of Business, Legal Services, Payroll Services, etc. For any further queries related to this or anything else visit TAXAJ

Watch all the Informational Videos here: YouTube Channel

TAXAJ Corporate Services LLP

Address: 1/11, 1st Floor, Sulahkul Vihar, Old Palam Road, Dwarka, Delhi-110078

Contact: 8961228919 ; 8802812345 | E-Mail: connect@taxaj.com

Related Articles

Letter of undertaking under gst for export

What does LUT under GST mean? LUT in GST: Full form/meaning is Letter of Undertaking. It is prescribed to be furnished in the form GST RFD 11 under rule 96 A, whereby the exporter declares that he or she will fulfill all the requirement that is ...What is GST registration for foreigners?

GST registration for foreigners is necessary for the non-resident taxable persons who are making taxable supplies in India. With India emerging as an economic powerhouse, a lot of non-resident Indias are willing to set up business in India. Hence, a ...How Do We Apply GST Number Online?

How to Register for GST GST Registration process is online based and must be carried out on the government website gst.gov.in. Every dealer whose annual turnover exceeds Rs.20 lakh (Rs.40 lakh or Rs.10 lakh, as may vary depending upon state and kind ...Complete knowledge of GST Registration, application & eligibility

GST Registration According to GST rules, it is mandatory for a business that has a turnover of above Rs.40 lakh to register as a normal taxable entity. This is referred to as the GST registration process. The turnover is Rs.10 lakh for businesses ...Supply to Special Economic Zone under GST

Meaning of Special Economic Zone (SEZ) A special economic zone (SEZ) is a dedicated zone wherein businesses enjoy simpler tax and easier legal compliances. SEZs are located within a country’s national borders. However, they are treated as a foreign ...