Statutory Audit Threshold FY 2026-27 — When does it become mandatory

🧾 Introduction

Many business owners and professionals confuse a Companies Act statutory audit with an Income Tax Audit under Section 44AB. While companies are generally required to have their financial statements audited every year under company law, tax audit applicability depends on turnover, gross receipts, and other conditions prescribed under the Income-tax Act.

For FY 2026-27 (AY 2027-28), understanding the applicable audit thresholds is essential to avoid penalties, delayed filings, and non-compliance with tax laws.

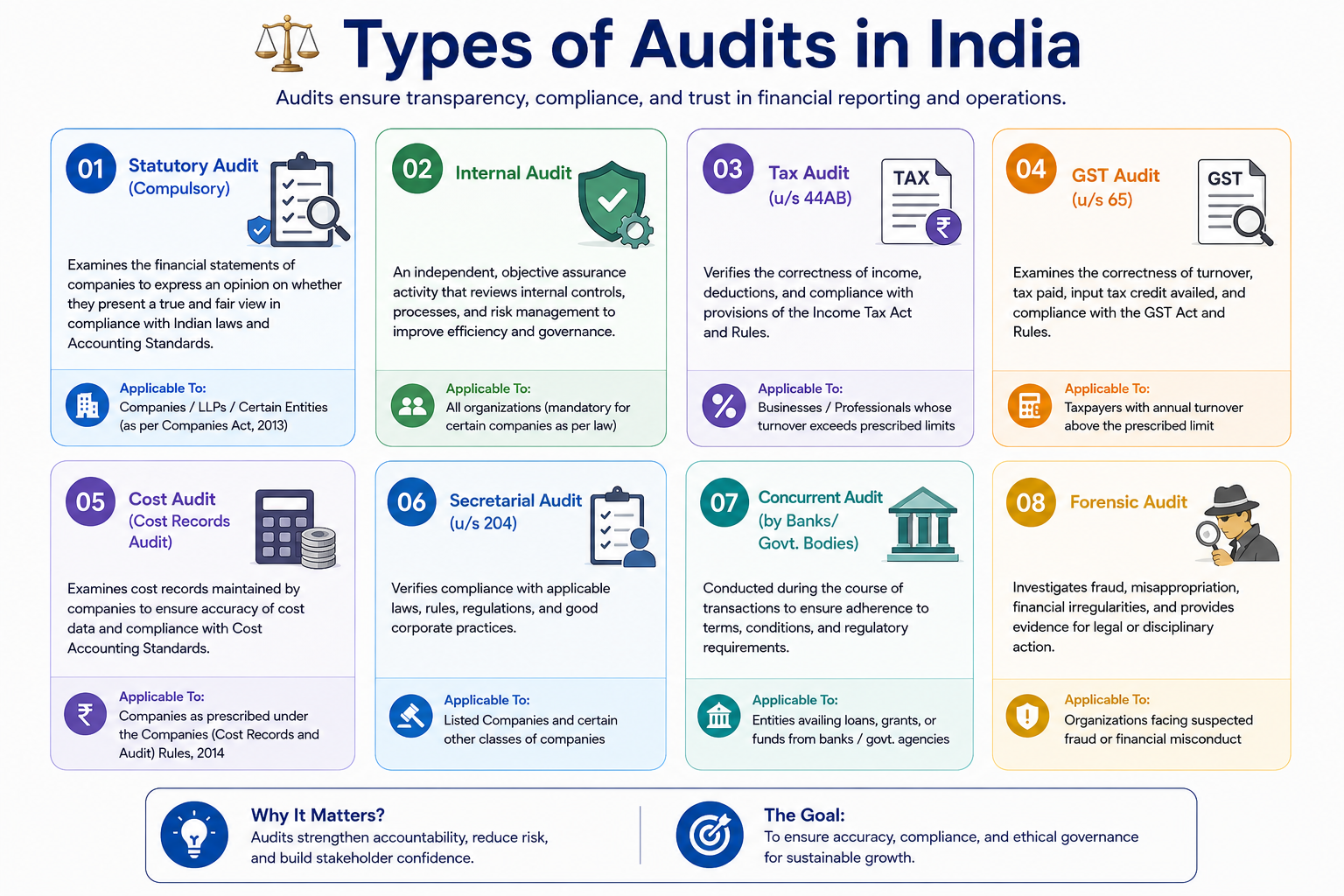

⚖️ Types of Audits in India

1️⃣ Statutory Audit (Companies Act)

1️⃣ Statutory Audit (Companies Act)

Applicable to:

- Private Limited Companies

- Public Limited Companies

- One Person Companies (OPCs)

Every company registered under the Companies Act is generally required to get its financial statements audited, irrespective of turnover or profit. There is no minimum turnover threshold for statutory audit of companies.

2️⃣ Tax Audit (Section 44AB)

Applicable to:

- Proprietorships

- Partnership Firms

- LLPs

- Companies

- Professionals

Tax audit becomes mandatory only when specified turnover or receipt thresholds are crossed.

📊 Tax Audit Threshold for Businesses (FY 2026-27)

Under Section 44AB(a):

| Category | Threshold |

|---|---|

| Normal Business | Turnover exceeding ₹1 Crore |

| Digital Business (Cash receipts and cash payments each not exceeding 5%) | Turnover exceeding ₹10 Crore |

A tax audit becomes mandatory if business turnover exceeds ₹1 crore. However, where cash receipts and cash payments are each within 5% of total receipts and payments, the enhanced threshold of ₹10 crore applies.

💼 Tax Audit Threshold for Professionals

Under Section 44AB(b):

| Category | Threshold |

|---|---|

| Professionals | Gross Receipts exceeding ₹50 Lakh |

Professionals such as:

- Chartered Accountants

- Doctors

- Lawyers

- Architects

- Consultants

- Freelancers

must undergo a tax audit if their gross professional receipts exceed ₹50 lakh during the financial year.

📌 Tax Audit for Presumptive Taxation Cases

Even if turnover is below the normal threshold, tax audit may still become applicable in certain situations.

Section 44AD (Business)

Tax audit may be required where:

- Income declared is lower than the prescribed presumptive rate; and

- Total income exceeds the basic exemption limit.

Section 44ADA (Professionals)

Audit may be required where:

- Income declared is below 50% of gross receipts; and

- Total income exceeds the basic exemption limit.

🏢 Statutory Audit Requirement for Companies

For companies, statutory audit is mandatory regardless of:

- Turnover

- Profit

- Number of transactions

- Business activity level

Even a newly incorporated private limited company with minimal transactions must get its accounts audited before filing annual ROC returns.

📅 Tax Audit Due Dates (FY 2026-27)

Generally, for taxpayers covered under Section 44AB:

| Compliance | Due Date |

|---|---|

| Tax Audit Report (Form 3CA/3CB & 3CD) | 30 September 2027* |

| Income Tax Return | 31 October 2027* |

(*Subject to any extension notified by CBDT.)

🚫 Consequences of Non-Compliance

Failure to get accounts audited when required can result in:

❌ Penalty under Section 271B

❌ Penalty under Section 271B

The penalty may be:

- 0.5% of turnover/gross receipts, or

- ₹1,50,000

whichever is lower.

📈 Practical Examples

Example 1 – Trading Business

| Particulars | Amount |

|---|---|

| Annual Turnover | ₹1.25 Crore |

| Cash Transactions | Significant |

✅ Tax Audit Applicable

Example 2 – Digital E-commerce Business

| Particulars | Amount |

|---|---|

| Turnover | ₹8 Crore |

| Cash Receipts | Less than 5% |

| Cash Payments | Less than 5% |

✅ Tax Audit Not Required

Since turnover is below ₹10 crore and cash transactions are within prescribed limits.

Example 3 – Consultant

| Particulars | Amount |

|---|---|

| Gross Receipts | ₹60 Lakh |

✅ Tax Audit Applicable

Because professional receipts exceed ₹50 lakh.

🌟 Key Compliance Tips

✅ Monitor turnover throughout the year

✅ Track cash receipts and payments separately

✅ Maintain proper books of account

✅ Reconcile GST turnover with financial statements

✅ Engage a Chartered Accountant well before the due date

✅ Review presumptive taxation eligibility annually

🏁 Conclusion

For FY 2026-27, every company registered under the Companies Act must undergo a statutory audit regardless of turnover, making audit compliance mandatory even for small private limited companies and startups. In addition, a tax audit under Section 44AB becomes mandatory for businesses with turnover exceeding ₹1 crore (or ₹10 crore where cash transactions do not exceed 5%) and for professionals with gross receipts exceeding ₹50 lakh.

Businesses and professionals should regularly monitor turnover, cash transactions, and presumptive taxation conditions to determine audit applicability well before year-end. Timely audits not only ensure legal compliance but also facilitate smoother tax filings, loan approvals, investor due diligence, and regulatory reporting.

📲 Stay Connected & Learn More

📞 Reach out via Call or WhatsApp: +91 8802912345

Related Articles

Mandatory Compliances for Private Limited Companies in Goa

? Introduction Goa, India’s smallest state by area but one of the most dynamic in terms of tourism and commerce, has been steadily attracting entrepreneurs and investors. The combination of a thriving tourism industry, a growing IT services sector, ...Statutory Audit Applicability — Turnover Thresholds FY 2026-27 (AY 2027-28)

Introduction Statutory audit compliance in India is often misunderstood, especially when it comes to turnover-based applicability. Many taxpayers confuse Statutory Audit under the Companies Act with Tax Audit under Section 44AB of the Income-tax Act, ...Statutory Registers — Mandatory Books Every Private Limited Company Must Maintain

Introduction Every Private Limited Company registered in India is required to maintain various statutory registers and records under the Companies Act, 2013. These registers serve as official records of the company’s ownership, management, charges, ...Tax Audit In India

The term ‘audit’ refers to a check, review, verification or inspection of a record, transaction, account etc. A tax audit is the process of verification and inspection of the accounts of a taxpayer to confirm their adherence to the provisions of the ...Tax Audit Limit under Section 44AB – Turnover Limits, Applicability, Due Date & Penalty (AY 2026–27)

Introduction A tax audit under Section 44AB of the Income-tax Act, 1961 is a mandatory compliance requirement for specified businesses and professionals whose turnover or gross receipts exceed the prescribed limits. The objective is to ensure that ...