Types of Form 16 in India

Form 16: The TDS Certificate for your Salary

Form 16 Part B

Form 16 Part B Form 16 Part A

Form 16 Part A

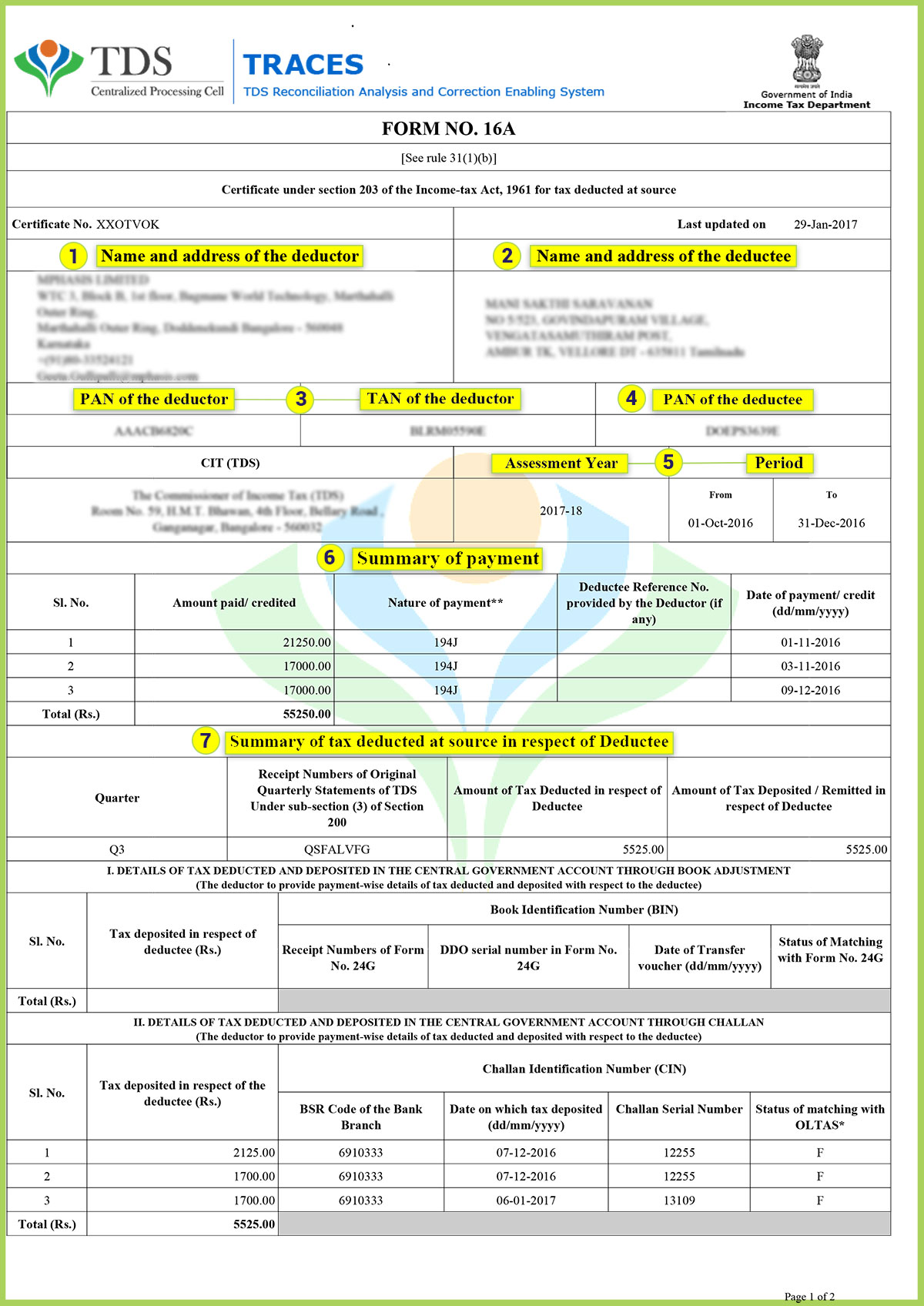

Form 16A: The TDS Certificate For Income Other Than Salary

Form 16B: The TDS Certificate for Sale of Property

Form 16B certifies that the tax has been deducted at source on the income earned from the sale of immovable property (building or a part of it/ land)

other than agricultural land. The TDS has been deposited by the property buyer with the Income Tax department.

According to the rules laid down by the Government of India, any person who purchases a property from a resident transferor needs to deduct tax at source on any money or consideration paid. TDS is deducted from all immovable property purchases in India. Immovable property is the property, including land or any building that does not include agricultural lands.

While employers and financial institutions require a TAN before they can deduct/ collect TDS, tenants and property buyers do not require a TAN. They can only furnish their PAN details while depositing the TDS with the government.

Related Articles

TDS (Tax Deducted at Source) return filing in India

Full form of TDS is Tax Deducted at Source. You may have experienced TDS in many forms - Bank FDs, salary payments to vendor payments, and TDS seem to infiltrate everywhere. Normally, TDS means an advance tax withheld by the payor from your income, ...Form 16 : TDS Certificate Form for TDS Credit

Form 16: Meaning Form 16 is an income tax form used by firms to give their employees information on the tax deducted. Form 16 is considered as the proof filing of income tax returns by your employer to the government. For example, if your income is ...Best TDS Software for CAs & Professionals in India

The thing which needs efficiency, precision and adherence to the laws of Tax Governance is called dealing with Tax Deducted at Source (TDS). TDS opposite on specific incomes required complete estimation and authenticity, indifference may point to ...How to File Form 15CA-15CB on Income Tax Site?

Brief Introduction with Their Importance As per Section 195 of the Income Tax Act 1961, every person liable for making a payment to non-residents shall deduct TDS from the payments made or credits given to non-residents at the rates in force. The ...Form 16 vs Form 16A: What’s the Difference?

? When it comes to income tax in India, two forms often confuse taxpayers — Form 16 and Form 16A. Both deal with TDS (Tax Deducted at Source), but they are not the same. Understanding them is key to accurate ITR filing. ? What is Form 16? Form 16 ...